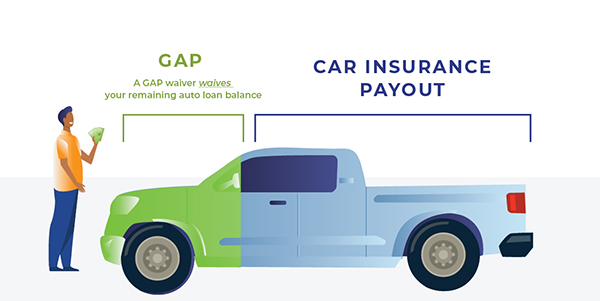

GAP waivers cover the gaps left behind by insurance payouts when your car is stolen or totaled.

Buying a car, whether it’s new or used, is an expensive investment. According to Experian, 84.6% of new cars and 54.6% of used cars are financed and 29.92% are leased. Whether you take out a loan or sign a lease agreement, you agree to be responsible for covering the initial cost of the car until it’s paid off.

But what happens if a texting driver isn’t paying attention and t-bones your car as you’re crossing an intersection? Your car insurance is supposed to kick in and cover what’s left to pay on your loan, right?

To an extent. When car insurance pays out, you’ll receive the equivalent of the car’s book value, or actual cash value (ACV), a calculation that takes into account your car’s age, depreciation, mileage, and other factors. Because of ACV, your auto insurance company isn’t guaranteed to pay out the full balance of your loan.

The responsibility for making up that difference falls fully onto you. Say bye to your savings, vacation fund, or planned down payment for a home — you’ve got to make up the difference on your loan balance somehow, after all.

Unless you’re covered by a GAP waiver.

GAP Waivers vs. GAP Insurance

“GAP” stands for Guaranteed Asset Protection, but that doesn’t necessarily mean a GAP waiver covers the gaps left behind by car insurance.

GAP coverage is sold in one of two forms: a GAP waiver or GAP insurance. Though both terms are often used interchangeably, there are some slight differences between each product: GAP waivers are offered and sold by your creditor or finance company when getting an auto loan or refinancing, whereas GAP insurance is a standalone insurance product that can be purchased at any time.

Both GAP waivers and insurance help to cover what you’re responsible for after car insurance pays out, but they function somewhat differently.

A GAP waiver waives the remaining loan balance — up to a specified percentage of your car’s loan-to-value (LTV), up to a specified amount. The LTV and max loan balance will vary by provider. For example, you may have coverage up to 150% of your car’s LTV, up to $50,000.

Car (LTV) Loan-to-Value Calculator

A loan-to-value ratio over 100% means you owe more on your loan than your vehicle is worth. An LTV over 125% can make it harder, but not impossible, to qualify for a refinance loan.

If your LTV is less than 100%, your car's value is higher than what you owe on your loan. The lower your LTV, the better.

Instead of waiving your remaining loan balance, GAP insurance functions similarly to car insurance. When you file a claim — and it’s approved — the insurance company backing your GAP insurance policy will pay out the remaining balance.

GAP waivers are paid for upfront when you take out a loan or refinance, and the cost of a waiver is commonly rolled into your auto loan. As a result, you’ll have coverage for as long as your loan remains in place, provided you adhere to the terms of your contract.

In contrast, GAP insurance is paid for monthly. Though this can be more convenient and budget-friendly, missing a payment or canceling your coverage can leave you solely responsible for paying the difference of your car’s remaining loan balance after auto insurance pays out.

What Happens When Your Car Is a Total Loss?

After a total loss or theft, your first step is to file a claim with your car insurance. Your insurance company will assess your car’s actual cash value using their proprietary calculation, taking into account the replacement cost of your vehicle minus its depreciation. Eventually, you’ll be paid out the car’s ACV, minus your insurance deductible.

Unfortunately, accidents, theft, and acts of nature happen unexpectedly. Just because your car purchase is recent doesn’t mean it’s protected from a total loss — in fact, your finances are likely most vulnerable when your loan is relatively new.

That’s because a car’s value depreciates over the length of time you own it. According to Edmunds, a new car loses an average of 11% of its value the moment you drive off the lot, and then 15% to 25% of its value each year over the next five years.

For example, imagine you just purchased and financed a brand new $30,000 car. That same car’s ACV drops immediately to $26,700 — an 11% drop equaling $3,300. Within a year, you can expect the car’s ACV to drop another 15% to 25%.

What does that mean for you? If at any point your car is deemed a total loss, your insurance will pay you its ACV. In the event you’re t-boned while driving that brand new $30,000 car off the lot, you could expect to receive a check for $26,700, minus $500 for your deductible. If your total auto loan balance was $30,000, you’d be left responsible for the remaining $3,800 — not exactly pocket change.

GAP waivers are intended to mitigate such a risk.

How GAP Waivers Work

Once your car insurance has paid out, it’s your GAP contract’s time to shine as long as you’re covered by collision or comprehensive auto insurance.

Once you begin the claims process, your coverage provider will determine your eligibility, and then waive the difference not covered by your car insurance, up to a certain percentage as specified by your waiver.

What Does GAP Cover?

Regardless of how or why your car is deemed totaled or stolen, your GAP coverage will pay out and bridge the gap between your car’s actual cash value and its remaining balance. Some GAP waivers will even cover the cost of your insurance deductible, up to a limit as defined by your contract.

Coverage isn’t insignificant, either. According to RateGenius data, the average GAP claim in 2019 was $3,410.23.

GAP coverage can be purchased for both new or used cars. However, some costs and situations are not covered by a GAP waiver, including:

- Remaining loan balances over a specified amount of your car’s loan-to-value ratio (This depends on your provider. For example, up to 150% LTV with a max of $50,000).

- Refundable additions made to your loan or lease contract, such as a vehicle service contract (VSC)

- Loan interest accrued after the date you lost your car

- Delinquent or past-due loan payments

- Late charges and other fees assessed after your loan inception date

- Cars purchased through private sales

What doesn’t GAP cover?

Though specifics vary depending on the specific product and provider, GAP waivers generally aren’t available for:

- Loan terms over 84 months

- Loans exceeding a defined limit (as set by the contract)

- Commercial vehicles or those with salvage or reconstructed titles

Additionally, GAP waiver coverage is limited to your original loan term. For example, if you refinance your car loan to a 36-month term and purchase a GAP waiver at that time, that waiver will only remain in force for those 36 months.

Also good to know: If you take advantage of a skip-a-payment promotion or otherwise miss a payment, your GAP waiver will not cover the cost of that missing payment or any interest accrued during that period.

According to RateGenius data, the average GAP claim in 2019 was $3,410.23.

Who Needs a GAP Waiver?

GAP waivers are a great way to protect against a hefty and unexpected expense after a crash, but they’re only useful when certain conditions apply. Situations in which you should purchase GAP coverage include when:

You put little to no money down

Putting money down on a new car purchase can increase the upfront cost of buying a car, but has long-term benefits. A down payment — ideally 20% or more — reduces your overall loan balance and the likelihood you’ll end up underwater while offsetting the effects of depreciation.

Without making a significant down payment, the depreciation that kicks in the second you drive off the lot can leave you exposed to out-of-pocket costs in the event your car’s stolen or totaled.

You have an upside-down loan

Upside-down car loans, or “underwater loans,” refer to situations in which your loan balance exceeds the value of your car, creating a high loan-to-value ratio. Totaling a car financed with an upside-down loan or high LTV would result in you owing more to the lender than your insurance would pay out to you.

You may also have an upside-down loan if you trade in a car you still owe on. Wrapping this “negative equity” into a new loan can, in turn, make your new loan upside-down.

Strive to maintain an LTV of 125% or lower. A lower LTV may make it easier to qualify for refinancing, and GAP waivers will not cover balances exceeding 150% of your vehicle’s LTV.

You drive a lot

High mileage can increase the rate at which your car depreciates in value. If you expect to put on more mileage than is average for your type of car, you may be faced with faster depreciation. This results in a decreased ACV for your vehicle and a smaller payout if your car’s a total loss.

Your new (or new-to-you) car depreciates quickly

Some vehicles depreciate quicker than others, particularly in the case of luxury models. Before buying a new car, research how quickly you can expect it to depreciate. Vehicles known for their usefulness, reliability, and resale value tend to depreciate more slowly and pose less of a risk to your finances in the event of a loss.

Your loan has a high interest rate

When you take out a car loan, the loan is made up of two parts: the loan principal and interest. The principal is the cost of taking out the loan, including your car’s value and any other products you choose to finance on top of it, such as a VSC. The interest is the cost of borrowing money.

Car loans are amortized, which means the bulk of your monthly payments go toward paying down the interest first. That means that for the first chunk of time you’re paying your loan, you’re not paying down much of the principal.

At the same time, your car’s ACV, which helps determine the initial principal of your loan, is steadily declining. Totaling a car before the loan has amortized means its ACV is no longer close to the loan’s principal, creating a “gap.”

Your loan term is at least 48 months

A car loan with a long term leaves you in a situation similar to having a high-interest loan. Because of the way car loans are structured, a longer loan term means it’ll take longer for you to build up equity. Without sufficient equity, you’ll still owe more on your loan than would be paid out based on your car’s ACV.

You’re leasing

Some lenders may require you to have some form of GAP coverage if you plan on leasing a vehicle. This is sometimes included as part of the lease agreement; in other cases, a product similar to GAP waivers, called loan/lease coverage, is included or offered.

How to Buy a GAP Waiver

GAP waivers are often sold as an optional addition to your loan (except in some cases, such as leasing). They may only be purchased at the time you take out a new loan or when you choose to refinance an existing loan and are offered by car dealerships and lenders (or their partners).

The waiver itself is a short addendum to your loan contract that lays out coverage terms and limits, the cost, your consumer rights, and other information. It’s signed at the same time as you sign the rest of your loan documentation.

Can I add GAP coverage if I already have a loan?

GAP waivers must be purchased at the same time you finance a loan. If you already have an auto loan but lack a GAP waiver, refinancing gives you the opportunity to buy a GAP waiver for the new loan (and probably even save a few bucks on the loan itself).

Average cost of a GAP waiver

Purchasing GAP waivers through a lender at the time of financing or refinancing costs an average one-time fee between $500 and $700. Like vehicle service contracts, that can be paid upfront or rolled into your auto loan. The latter option may be more affordable than paying for the waiver all at once, but you will end up paying interest on the cost of the waiver.

Can I cancel GAP coverage and get a refund?

Unless GAP is required by your lender, you’re always able to cancel coverage. This is particularly useful when your loan balance falls below the actual cash value of your vehicle. However, if you still owe more than your car’s worth, canceling coverage will expose you to potential out-of-pocket costs if your car’s ever totaled or stolen.

Before buying a GAP waiver, or if one’s already in place, look over its cancellation terms to figure out how refunds are handled. Sometimes, canceling within a certain amount of time (usually 30 to 60 days) will result in a full refund; if your contract was paid for upfront but has been in place for a while, you may still receive a prorated refund.

If you rolled your GAP waiver into your auto loan or refinance loan, your lender will be the named payee on any refunds unless a paid-in-full letter is provided.

Are GAP Waivers Worth It?

Dealing with a total loss is a headache in and of itself. Receiving an insurance payout that’s less than what you owe on your loan is enough to frustrate anyone, especially when you’ll need to scrape together a couple hundred to a couple thousand dollars as a result.

GAP coverage makes sense in any situation where your loan payment is likely to be larger than your car’s actual cash value. Whether you’re financing a new vehicle purchase or refinancing an existing loan, consider getting GAP coverage to offset depreciation — particularly if your car is likely to depreciate faster than average.

;)