Rate shopping doesn’t need to be like balancing on a tightrope.

When you think of shopping, your mind probably jumps to browsing your favorite clothing brands — not shopping for the best interest rate.

The idea of rate shopping for an auto loan or home loan doesn’t sound super exciting. Filling out paperwork, communicating back-and-forth with potential lenders — it’s a time commitment. But you compare prices for purchases all the time — cars, furniture, groceries, clothing, you name it. Why not compare interest rates?

It could save you thousands of dollars.

Before you start comparing rates and submitting loan applications, you need to understand the fundamentals of rate shopping — like how it could impact your credit score.

Rate shopping is the process of researching various lenders and comparing loan rates — particularly for car loans and home loans. It’s like comparing the price of a certain car at one dealership versus other dealerships across town.

When rate shopping, you might submit several loan applications. For example, to land the best rate, you might apply for an auto loan with three separate lenders. This helps you determine the best rate and lender.

These are typically large loans, so even a slightly lower rate can save hundreds (or even thousands) of dollars over the life of the loan.

What Are the Benefits of Rate Shopping?

As you can imagine, the biggest benefit of rate shopping is saving a lot of money.

Here’s an example. Let’s assume you’re in the market for a new car. You want to finance your purchase with a $30,000 car loan, so you start comparing loans. The first lender you come across offers a 60-month loan with an interest rate of 5%, which equates to monthly payments of $566.

Instead of calling it a day, you check out a few more lenders. One particular lender happens to place a lot of importance on credit scores (more so than the average lender) — and they like your 725 credit score. They’re willing to offer you a 60-month loan with a 4% interest rate. That’s a monthly payment of $552.

It might not seem like a big difference, but, over a 60-month period, that’s $840.

For mortgages, the financial benefits are even larger. Let’s assume you’re buying a new house, and you’re financing it with a $450,000 mortgage. You narrow down your search to two lenders. Both lenders offer you a 30-year mortgage, but Lender A’s interest rate is 4.25% while Lender B’s interest rate is 4%.

Lender B’s offer saves you $1,980 over the life of the loan. A few hours of work is worth a couple of thousand dollars, don’t you think?

In addition to saving money, rate shopping allows you to compare lenders too. This enables you to consider other important factors, such as customer service, loan processing times, and communication skills. Saving a few hundred dollars with one lender may not be worth it to you if the trade-off is terrible customer service.

So, rate shopping lets you find the best interest rate and lender for your needs. Whether you test the waters with one lender or several, you’ll have to be cautious of credit inquiries.

A credit inquiry is an authorized request to look at your credit report. In other words, when you submit a loan application, you allow the lender to contact a credit bureau (such as Equifax) and “inquire” for a copy of your report. But not all credit inquiries are the same. There are two types:

Hard inquiries

Soft inquiries

Hard inquiries can affect your credit score, while soft inquiries do not. Whenever you check your own credit report, that’s considered a soft inquiry. Whenever a potential lender checks your credit report, that’s considered a hard inquiry.

So, if you apply for an auto loan, mortgage, or new credit card, a hard inquiry will be added to your credit report.

When rate shopping, you’re dealing with loan applications — so, hard inquiries come into play. Since hard inquiries can affect your credit score, it’s important to be deliberate with your loan applications.

Too many hard inquiries will ding your score. On average, each hard inquiry decreases your credit score by 5 to 10 points. That being said, only inquiries over the last 12 months impact your current score. After two years, inquiries are removed from your credit report altogether.

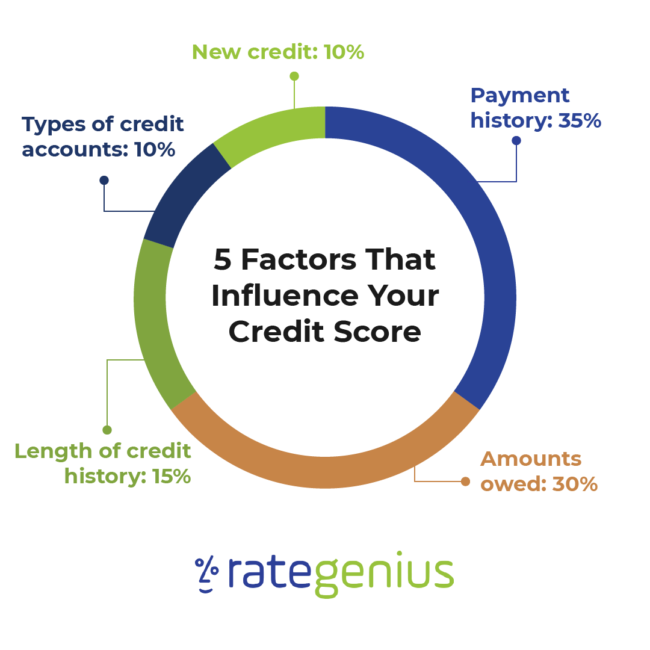

Lenders track the “new credit” portion of your score to gauge your riskiness as a borrower. If you submit a flood of loan applications (especially for different types of loans), you’re indicating to lenders that you might be financially unstable — and high risk.

On average, each hard inquiry decreases your credit score by 5 to 10 points.

But, you might be wondering, “How am I supposed to compare and apply for multiple loans when I’m rate shopping without hurting my credit?”

Don’t worry! The two main credit scoring models, FICO and VantageScore, consider this conundrum when you’re applying for loans. As long as you batch your loan applications into specific periods of time, your credit score will only reflect one hard inquiry.

However, FICO and VantageScore have different rate shopping windows and rules.

The first represents any hard inquiries related to rate shopping within the last 30 days. The 45-day window deals with any batches of rate-shopping inquiries that are older than 30 days.

Let’s say you start your rate shopping journey today by sending in your first application. If you find a loan within 30 days, the inquiries won’t impact your credit score while you’re comparing rates. In other words, you could apply for five car refinance loans from five lenders over the next 30 days — and your FICO score will ignore these applications.

But, on day 31, if you apply for a sixth auto loan, your FICO score will reflect the loan application from day one — and the sixth lender may receive your updated score, which would include the first hard inquiry.

On top of that, your FICO score will also consider periods of rate-shopping inquiries older than 30 days. For these inquiries, FICO’s rate shopping window is 45 days.

So, let’s assume you were rate shopping for an auto loan six months ago — but you managed to confine your loan search to 42 days. Your credit report will show each hard inquiry, but only one will count towards your score since it was within a 45-day window. Had your search extended to anything beyond 45 days, your credit score would be impacted by multiple hard inquiries from six months ago.

It’s important to note that these rate shopping windows only apply to auto loans, student loans, and mortgages. Multiple credit card inquiries will not be considered as a single inquiry.

According to FICO, 90% of lenders use FICO Scores when reviewing loan applications. However, when you’re applying for a loan, you can’t know for sure which credit scoring model is being used. So, it’s important to consider VantageScore’s rate shopping conditions too.

VantageScore’s rate shopping window is 14 days — which is considerably shorter than FICO’s.

However, VantageScore doesn’t limit rate shopping to auto loans, student loans, and home loans. For example, (although we don’t advise it), you could apply for four credit cards within a two-week span, and VantageScore would still register your credit card application spree as one hard inquiry. In other words, your credit score would only reflect one hard inquiry, even though all four credit card applications would show up on your credit report.

That being said, reexamining our previous example, if you applied for five auto loans over a 30-day period, your VantageScore would register multiple applications.

So, to appease both models, you’ll need to limit your loan application period to 14 days.

‘New credit’ only represents 10% of your score, so a couple of hard inquiries won’t tank your score.

It’s not the end of the world if you can’t contain your search to a 30 or even 45-day span. “New credit” only represents 10% of your score, so a couple of hard inquiries won’t tank your score.

Plus, your credit score isn’t the only factor that lenders consider when you apply for a loan. For example, when refinancing a loan, lenders also consider your income, loan-to-value ratio, and debt-to-income ratio.

Before you dive in, keep these rate shopping tips in mind.

Apply within a two-week window

If you can, shorten your loan application period to 14 days. By doing so, you’ll ensure that only one hard inquiry factors into your credit score. For whatever reason, if that’s too tight of a window, try to at least stay within 45 days. VantageScore will consider anything beyond 14 days as a separate shopping event, but your FICO score will only register one hard inquiry if you knock out your loan applications within 45 days.

Stick to one type of loan

For it to be considered rate shopping, you can only apply for one type of loan. Otherwise, your credit score will be impacted by multiple credit inquiries. You can’t sneak one loan type into a batch of another type. For instance, if you apply for three car refinance loans and a mortgage within a ten-day period, that’s considered two separate shopping events — and two hard inquiries.

Use the same loan amount

To avoid confusion, keep your loan amounts consistent across applications. If you’re trying to take advantage of rate shopping, you don’t want credit reporting agencies to think you want multiple loans.

The Bottom Line

Rate shopping is a time commitment, but it will help you find the best interest rate for a car loan, refinance loan, or mortgage loan. To leverage this approach and maintain your credit score, limit your loan application window to within two weeks.

Gather as much information as possible beforehand to maximize your time. That way, you’ll avoid multiple hard inquiries.

Credit checks are a foundational part of lending and underwriting. Whether applying for a credit card, auto loan, mortgage, or refinancing an existing vehicle loan, lenders evaluate credit information to determine risk. The difference between a soft pull and a hard credit inquiry can influence approval decisions, interest rates, and even short-term credit score movement.…

Auto loan refinancing became increasingly common in 2025, driven less by short-term market timing and more by changes in how consumers managed long-term debt. Borrowers who financed vehicles during the high-cost years of the early 2020s revisited their loans, often finding opportunities to reduce monthly payments, improve loan terms, or better align debt with their…

Choosing where to finance a vehicle can make a significant difference in the total cost of ownership. While banks and dealerships still dominate car lending, credit unions have steadily earned their place as the go-to choice for drivers seeking lower rates, flexible terms, and trustworthy service. Because they operate as member-owned, not-for-profit institutions, credit unions…

;)